Most engagement strategies still treat customer touchpoints like a set of disconnected campaigns.

A loyalty program lives in one place. Offers live in another. Membership access is handled somewhere else. Identity is tied to a CRM record that customers never see. And the “experience” is stitched together through emails, SMS, app prompts, and PDFs that expire the second someone closes the tab.

Mobile wallets flip that model.

When a customer saves a pass into Apple Wallet or Google Wallet, the wallet stops being a one time delivery channel. It becomes a persistent customer layer, one that can hold loyalty, offers, membership, and identity in a single place that customers already check when something matters.

That is what makes the wallet powerful at scale. Not just reach. Continuity.

Why “System of Record” Matters in Engagement

In IT, a system of record is where the truth lives. It is the canonical source that other systems reference. In customer engagement, most brands do not have that.

They have records, sure. CRM data. Purchase history. Email engagement. App sessions. But customers experience none of it as a unified layer. They experience fragments.

A wallet pass changes the shape of the relationship:

- It persists on the customer’s device

- It stays current through updates, not reminders

- It centralizes key engagement objects like tier status, rewards, offers, member ID, barcode, and access credentials

- It ties operational systems to customer facing reality in a way that is measurable and repeatable

Instead of constantly trying to drive customers back into a channel, the wallet becomes the place where your relationship is stored and refreshed.

What About Apps?

Most enterprise brands already have an app. In many cases, that app can technically store loyalty balances, membership details, and offers.

The difference is adoption and behavior.

Apps are destinations that customers use when they are motivated. They require a download, regular engagement, and ongoing maintenance to stay relevant. For some brands, especially those with strong weekly usage, that works.

Mobile wallets behave differently.

Wallets are utilities. They are designed for instant access, simple interaction, and persistent visibility. A loyalty ID, membership credential, or offer does not require navigation or login. It is simply there when the customer needs it.

That is why wallets work so well as a persistent customer layer for loyalty, offers, membership, and identity, while the app remains the right place for deeper experiences like shopping, account management, service, and content.

This is not wallet versus app.

It is wallet as the utility layer that reduces friction and increases participation across the entire ecosystem.

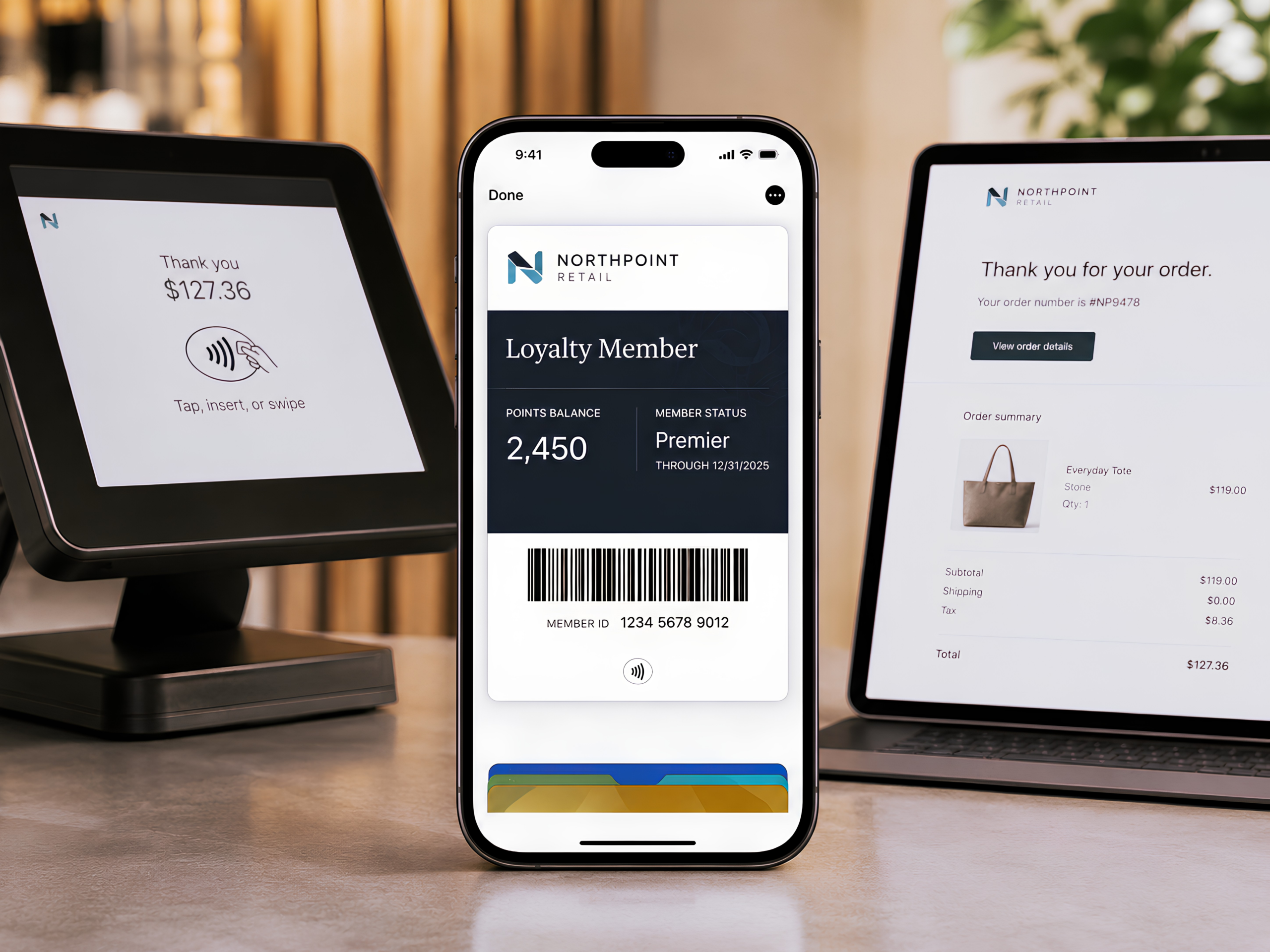

What Actually Lives in This Customer Layer

Think of the wallet pass as a living record, not a coupon image.

Depending on the program, it can hold:

Loyalty

- Points and balance

- Tier status and progress

- Reward eligibility

- Location specific perks

Offers

- Personalized promotions

- Expiration logic and eligibility rules

- Offer history and redemptions

Membership

- Member identification and access

- Renewal dates

- Location based entry or benefits

Identity

- Customer identifiers mapped to backend systems

- Scannable barcodes or QR codes for in store and onsite use

- Verified credentials for controlled access scenarios

The key is that the wallet makes these elements feel like one coherent asset.

Customers do not think in terms of channels. They think in terms of what they need at that moment.

The wallet aligns with that behavior.

Operational Advantages at Enterprise Scale

If you position mobile wallets as just another marketing channel, you miss the larger opportunity.

The bigger win is operational.

Wallet programs reduce the number of engagement surfaces your team has to manage and simplify the mechanics of keeping customer facing information current.

Some of the operational advantages that show up quickly:

- Fewer touchpoints to maintain

- No need to rebuild loyalty dashboards inside an app just to show tier and points

- No need to distribute static barcodes or reissue physical cards

- Fewer “I forgot my login” or “I lost my card” moments

- Faster rollout across regions, franchises, and brands

- Centralized updates that do not require app releases

Enterprise engagement fails when the workload becomes too manual to sustain. The wallet reduces that overhead and creates a more durable structure.

Data Advantages When the Wallet Becomes the Canonical Customer Surface

Most teams have data everywhere, but little clarity about what is truly driving engagement.

Wallet programs create a cleaner data loop because the object itself is persistent and measurable.

That unlocks meaningful advantages:

A more stable engagement signal

You can understand behavior over the life of the pass, not just a single campaign click.

Stronger first party data alignment

The wallet pass can serve as a consistent identifier that maps cleanly to CRM and marketing systems.

Cleaner experimentation

Messaging, segmentation, and offers can be updated centrally without rebuilding entire experiences.

More accurate real world attribution

Wallet passes bridge online engagement with offline actions like in store redemption, event entry, or member validation.

When the wallet is treated as the persistent layer, engagement data becomes less fragmented and more actionable.

Moving Beyond Campaign Bursts

Many brands can create moments. They can launch a promotion, run an event, announce a new tier, or push a seasonal offer.

But the experience resets after each moment because there is no persistent home for the relationship.

That is the difference between marketing as a series of bursts and engagement as a compounding system.

A wallet pass compounds because it stays present.

Every update builds on an existing saved asset. Every offer extends the relationship. Every new benefit strengthens a layer that is already there.

That is what makes the wallet feel like a system of record.

It is not just where you send a message. It is where the customer relationship lives.

The Bottom Line

Mobile wallets are not just replacing plastic cards or supporting campaigns.

They are becoming a practical system of record for customer engagement because they unify loyalty, offers, membership, and identity inside a customer controlled environment that is always accessible and always current.

For enterprise teams, that translates into simpler operations, cleaner data loops, and more durable engagement over time.

If you want to see how mobile wallets can support enterprise scale engagement across loyalty, membership, offers, and ongoing communication, Book a demo to see how Bambu Wallet helps enterprises and growing brands deploy scalable mobile wallet programs inside Apple Wallet and Google Wallet, or follow us on LinkedIn for more insights.